Introduction and Theoretical Framework

In the last two decades, several jurisdictions around the world have reformed or are considering reforming their corporate insolvency and restructuring laws1 in order to promote legal regimes that are conducive to restructuring viable companies. Many jurisdictions, including significant economies in Asia, have court-supervised corporate restructuring frameworks that are drawn from Chapter 11 of the Bankruptcy Code 1978 (Chapter 11) in the United States (US) and/or schemes of arrangement or administration process in the United Kingdom (UK).

It is widely agreed that the key goal of corporate restructuring law is to preserve, as much as possible, the debtor company’s viable (but financially distressed) business at the beginning of the restructuring process until it exits the process, and thus it is critical for the transaction costs to be minimised. Once the restructuring is resolved speedily and in a cost-efficient manner, capital and labour can be put to productive uses quickly. Companies that are no longer economically viable should proceed to liquidation. Further, even though restructuring is a relatively rare occurrence among businesses, the outcomes of restructuring have ex ante effects on the credit market since costly restructurings may lead to attempts by the creditors to avoid the process and instead charge high interest rates to compensate for their costs, or demand more collateral. Some of the early debates on agency costs of debt and inefficiencies in bankruptcy include Jensen and Meckling,2 Baird,3 Jackson,4 Bebchuk,5 Aghion, Hart and Moore,6 and Bradley and Rosenzweig.7 Bankruptcy scholars, particularly the economically minded scholars, view the goal of restructuring law to be solving the coordination problem of the creditors. Under their normative Creditors’ Bargain Theory, creditors may in their own self-interest prefer to race to grab the assets of the debtor in financial distress when they are better off bargaining over how the assets should be best used, and Chapter 11 is to solve their coordination or collective action problems.8

The model adopted by Chapter 11 in the US for restructuring is that of a single gateway, and is a debtor in possession model (DIP) where the management of the debtor continues to drive the restructuring post-filing of the petition, with the process ultimately being approved by the court. In the UK, the legislative approach allows for four gateways for restructuring: the scheme of arrangement, administration, the restructuring plan and company voluntary arrangement (CVA). The English scheme of arrangement9 is a DIP model for early stage restructuring but the secured creditors retain significant rights to veto the restructuring and the administration process requires the insolvency practitioner to be in control of the restructuring, and thus the administration is a practitioner-in-possession (PIP) model.10 The third is a recent addition that was introduced by UK Corporate Insolvency and Governance Act 2020; it is closer to Chapter 11 and shares many of its features. The CVA allows for a company to restructure its debts by compromising with certain creditors, and it is led by its directors unless the company is in liquidation or in administration.11 In the UK, only the English scheme and restructuring plan (but not administration or CVA) require court approval. In this book, I will not focus on the CVA as the CVA is subject to minimal court involvement.12

The US Chapter 11 and the English schemes and administration have been influential in the exportation of their insolvency and restructuring laws globally. I refer to both the US and the UK systems as the ‘Anglo-American’ models, whilst recognising that there are differences between the two models in bankruptcy law. Four economically significant jurisdictions in Asia – Mainland China, India, Hong Kong and Singapore – are no exceptions. They have also recently reformed or are considering reforming their corporate restructuring laws to promote regimes conducive to restructuring financially distressed but otherwise economically viable companies, and draw concepts from the US and the UK. This book focuses on the restructurings of large distressed companies in the four Asian jurisdictions.

Both Hong Kong and Singapore are international financial centres in Asia. Mainland China and India rank second and sixth globally respectively in the terms of the nominal gross domestic product (GDP) in 2021.13 These jurisdictions continue to adhere to a framework that requires the court’s final approval but draw references from US Chapter 11 and/or the English schemes or administration. Singapore’s 2017 reforms to the insolvency and restructuring framework are the closest to Chapter 11. Mainland China, India and Hong Kong (in its proposed corporate rescue bill) have not adopted the full DIP regime, and insolvency practitioners continue to play an important intermediary role. These jurisdictions have very different governance structures and institutional frameworks from the origin jurisdictions. For instance, the shareholdings of large companies in Asia are far more concentrated and the debt that is sought to be restructured is often not identical to the US/UK restructurings.

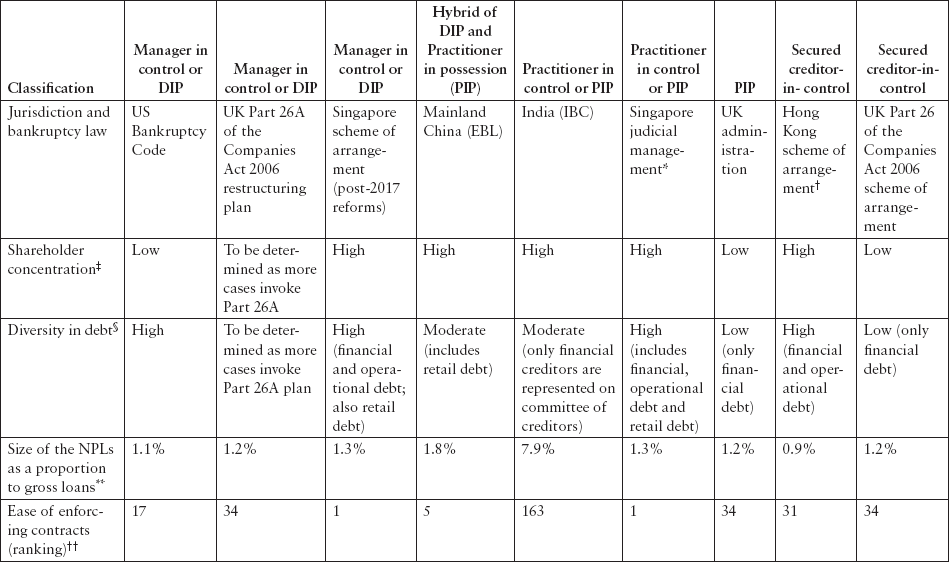

The taxonomy of the comparisons of the various court-supervised models in the US, UK and each of the four Asian jurisdictions in Table 1.1.

Given the core aim of restructuring law is to preserve the business of financially distressed but otherwise viable business, the key motivation of the book here is the design of restructuring law and policy for large companies in Asia that minimises these transaction costs. These ex post transactional costs include the professional costs of the advisers and the administrative fees, costs to creditors in terms of time value of money, and the loss of opportunities that may arise if stakeholders are disincentivised from putting forward competing viable restructuring plans. Ex ante costs, which include loss of managerial time and increased overall cost of debt, are more difficult to quantify. Empirical studies have been carried out to isolate the effects of the impact on cost of lending involving a regime change (eg for Italy)14 or using direct bank data on the interest rate chargeable on debt for the financially distressed firms.15 However, this book will only be concerned with ex post costs.

In this book, I have concentrated only on large companies. The choice of restructurings of large companies is driven by the fact that the restructuring regimes are much more complex than those applicable for small and medium-size enterprises (where the owners and managers are the same persons). Inevitably, there is no standard definition of large companies across the Asian jurisdictions and the criteria is driven by both functions as to data availability and the amount of debt that is involved. For three of the four Asian jurisdictions studied in the book, I consider large companies to be those that are listed on a stock exchange and/or issue publicly traded debt. This is the criteria that is used for Mainland China, Singapore and Hong Kong. In these jurisdictions, often financial and other data is only available for listed companies and those that issue public debt because of the disclosure requirements imposed by the various stock exchanges or interest in the press due to their significance to the economies. For India, more information is available on the companies undergoing the resolution process pursuant to the Indian Insolvency and Bankruptcy Code 2016 (IBC) disclosed by the regulator, that is, the Insolvency and Bankruptcy Board of India (IBBI). In this book, large companies in the Indian context are those where the size of the financial claims is at least INR100 million (US$1.3 million). Throughout the book, to ensure comparability, I have attempted to convert the local currency in each of the four jurisdictions to US dollars.

Table 1.1Models of debt restructuring systems

* Judicial management can be within or out-of-court in Singapore. The out-of-court judicial management regime came into force via Insolvency, Restructuring and Dissolution Act 2018 on 30 July 2020.

† Excludes the soft-touch provisional liquidation that is used in Hong Kong.

† Assessment on shareholding concentration East Asian jurisdictions (Hong Kong and Singapore) is based on Chen and Wan (2018) (based on a sample of 25% of the companies that were listed on SGX during 2009–15; the mean of shareholding interests of the largest beneficial holder was 40.7%; based on a sample of 25% of the companies that were listed on Stock Exchange of Hong Kong (SEHK) during 2009–15; the mean shareholding interests of the largest beneficial holder was 45.98%). For India, I use U Varottil, ‘The Nature of the Market for Corporate Control in India’ in Varottil (2017) Table 11.5 (showing that, as of 31 March 2015, the average promoter shareholding of companies on CNX Nifty (50-stock index representing about 66.2% of the free float market capitalisation of stocks listed on NSE), CNX 100 (100-stock index representing 78.57% of the free float market capitalisation of stocks listed on NSE) and CNX 500 (representing about 95.77% of the free float market capitalisation of stocks listed on NSE) is 49.22%, 52.17% and 54.62%, respectively). For China, I use Jiang and Kim (2014) (data showing that, as of 2012, for the non-financial firms listed on Shanghai and Shenzhen stock exchanges, the largest shareholder held on average 36.8% of the shareholding and the five largest shareholders together held 53.2% of the shareholding).

§ Assessment on diversity in debt-holdings is based on the following: (1) for Singapore, assessment is based on the dataset of schemes of arrangement in Appendix D; (2) for Hong Kong, based on the dataset of judgments involving schemes of arrangement in Appendix C; (3) for India, based on the analysis of the dataset on the CIRPS in Appendix B; (3) US and UK data from Ivashina et al (2018).

** Figures from World Bank, as at 2020.

†† Figures from World Bank ‘Doing Business 2020’. The World Bank announced that the ‘Doing Business’ reports would be discontinued on 16 September 2021 due to data irregularities. However, the figures are included here as the irregularities did not pertain to the indicators relating to enforcing contracts but to ‘Starting A Business’, ‘Legal Rights – Getting Credit’ and ‘Paying Taxes’. See RC Machen, MT Jones, GP Varghese and EL Stark, ‘Investigation of Data Irregularities in Doing Business 2018 and Doing Business 2020 – Investigation Findings and Report to the Board of Executive Directors’ (Wilmerhale, 15 September 2021) 1–16, available at thedocs.worldbank.org/en/doc/84a922cc9273b7b120d49ad3b9e9d3f9-0090012021/original/DB-Investigation-Findings-and-Report-to-the-Board-of-Executive-Directors-September-15-2021.pdf.

In US/UK scholarship, the restructuring process is traditionally characterised as either ‘management-driven’ (also known as debtor in possession)16 or ‘management-displacing’ (also known as practitioner in possession).17 As mentioned earlier, the DIP model is associated with the US Chapter 11 proceedings. In the latter, found primarily in the UK, it is also characterised as secured creditor-driven, particularly if secured creditors have a floating charge over all or substantially all of the assets of the company and may proceed appoint receivers to take over control of the collateral with a view of sale.18 The DIP model is associated with a bias towards favouring reorganisation and the secured creditor-driven process has a pro-liquidation bias. The debates have centred on the trade-offs and optimal design of restructuring law and policy in addressing agency and coordination costs of various market participants in either model, and the literature has been updated to include modern bankruptcy practice by several scholars, including Skeel,19 Baird and Rasmussen,20 Skeel and Triantis,21 and Paterson.22 The PIP model was also discussed when the UK introduced administration as a gateway to restructuring in 2002 where the insolvency practitioner takes control of the restructuring.

However, the debates are largely located in the US/UK, focusing on the optimal structures in these two advance jurisdictions. With certain exceptions of emerging jurisdictions23 and jurisdiction-specific studies,24 there has been less focus on optimal designs of restructuring law in emerging jurisdictions, even though more emerging jurisdictions are favouring processes that promote reorganisation. Insolvency and restructuring law are also seen as a means to resolve a jurisdiction’s non-performing loans so as to ensure the stability of its banking sector. In contrast, there is influential theoretical and empirical scholarship on addressing agency costs in corporate governance structures in Asia for solvent companies.25 Insofar as the empirical evidence on insolvency and restructuring law, while there are English language monographs on jurisdiction-specific studies particularly on Mainland China, they have limitations in demonstrating how these frictions in the relationships matter in modern bankruptcy practice. For instance, Zhao focuses only on listed company reorganisations26 and does not cover bond restructurings, which have drawn significant attention due the high-profile nature of these defaults on the wider economy and their implications on the future of bankruptcy reforms.27 Since Zhang’s work on reorganisations of Chinese firms up to 2015, the Chinese Government has taken a number of measures to use bankruptcy law to facilitate market reforms.28 Mrockova discusses comprehensively the implementation of the Chinese Enterprise Bankruptcy Law 2006 based on extensive interviews with various stakeholders but does not address in-depth the diverse interests of creditors.29 Additionally, none of the above authors deal with how reorganisations are impacted by the solutions of the jurisdictions in resolving non-performing loans.

In view of the differences in the share ownership and debt structures between Asian firms and the US/UK firms, as well as the differences in the legal institutions, the question arises as to whether the solutions adopted in the US/UK to respond to the agency and coordination costs posed by frictions of stakeholders in fact work as intended when transplanted to Asia. This book fills the gap by reference to experiences in Asia. The key contribution of this book is the analysis of the solutions adopted by corporate restructuring law and practice in the US and the UK that address the agency and/or coordination costs posed by frictions in shareholder–creditor, manager–creditor and creditor–creditor relationships, and how these costs have limitations in the context of Asian companies. These solutions also do not adequately consider the variations to the agency and coordination costs posed by the banking regulator’s interests in resolving non-performing loans in emerging jurisdictions, the benefits and limitations of the independent gatekeepers operating in the insolvency ecosystem, and the complex relationships between corporate restructuring law and other areas of the law.

The central thesis of this book is that an optimal design must take into account the following that are absent or not present to the same extent as in the US/UK: (1) the interaction between concentrated shareholdings and widely held debt leading to significant risks of prejudice to outside creditors; (2) the incentives of the state in resolving non-performing loans for the purposes of bank regulation; (3) the benefits and limitations of the independent gatekeepers, being the insolvency practitioners and the courts; and (4) the interaction among restructuring law, enforcing contracts and duties of directors of financially distressed companies.

1.2.RESTRUCTURING MODELS IN ANGLO-AMERICA AND ASIA

1.2.1.The US Pure Debtor in Possession Regime

The US Chapter 11, a DIP regime, is widely regarded as pro-debtor and pro-restructuring, and is highly flexible.30 In particular, Chapter 11, the choice for large firm restructurings,31 is designed to encourage efficient consensual bargaining by parties to maximise the debtor’s assets and minimise the collection costs of creditors.32 To this end, a set of comprehensive tools are in place. The debtor management remains in possession and the debtor has a strong automatic stay or moratorium33 while the management has an exclusive right to propose a plan of reorganisation for the first 120 days of the case (which can be extended).34 During this period, committees of creditors negotiate the plan, supported by a mandatory disclosure regime, as to how the assets are to be deployed. Other tools include prohibiting the exercise of termination rights of non-financial contracts as a result of filing for Chapter 11 or ipso facto clauses,35 and allowing the creditors to cherry-pick certain executory contracts.36

Creditors’ and/or shareholders’ hold-outs on how assets are to be distributed are addressed by the court’s ability to impose a cram-down, either within-class or by way of a cross-class cram-down.37 Chapter 11 requires the impaired creditors to be classified according to their rights for voting purposes. When the majority of the creditors represent two-thirds in value in each class vote for the plan, the plan is binding on the minority of the class.38 For the cross-class cram-down to be exercised, even if not all of the impaired classes vote for the plan, certain conditions must be satisfied. The plan must not discriminate unfairly and the plan must be fair and equitable.39 The latter is satisfied if the absolute priority rule (APR) found in distributions in liquidation – that is, requiring that senior classes must be paid in full before junior classes can receive any payment in the absence of consent by the class in question – is respected. Other conditions include satisfying the ‘best interests’ test, that is, the creditor must receive at least what he/she would be otherwise be entitled to in the liquidation.40 In theory, shareholders of a company that is insolvent should be wiped out if the APR is strictly applied. DIP loans or rescue financing is well established in Chapter 11, where providers of the DIP financing may be existing lenders or new lenders, and may have their priority elevated to other creditors with the court’s approval.41

In the UK, there are two possibilities for effecting a restructuring using a court-approved process. In addition, the debtor may also restructure under the administration framework pursuant to the Insolvency Act 1986 (amended by the Enterprise Act 2002), which allows for the appointment of administrators by the court. In the case of administration, it is also possible to appoint the administrator with an out-of-court process.

For restructuring that is to be ultimately approved by the court, Part 26 of the Companies Act 2006 (in existence at least since 1870)42 provides only for a within-class cram-down for the English schemes of arrangement. In 2020, the new restructuring plan was introduced in Part 26A of the Companies Act 2006 via the Corporate Insolvency and Governance Act 2020 (CIGA), which has many of the Chapter 11 features described below.

In a traditional English scheme of arrangement, which model was transplanted to India, Hong Kong and Singapore, there are three stages to the approval process. First, the company applies to the court to convene a meeting of creditors. Second, the relevant class meetings are held and the scheme must be approved by a majority in number representing 75 per cent in value of the creditors within the class, in order to effect a within-class cram-down. Third, the scheme must be approved by the court for it to be effective.43 In reviewing the fairness of the scheme, the court will normally give effect to the wishes of the creditors so long as the classes of creditors are properly formed, though the court does not serve as a rubber-stamp.

To effect a cross-class cram-down and to squeeze out the junior creditors and shareholders, the process is more complex and involves the English scheme being twinned with the English administration in a pre-packaged plan.44 The English or English-modelled scheme is a DIP model but is classified as a secured creditor-in-control model, as there is no ability to stay enforcement by secured creditors against their consent while the debtor is attempting to seek a restructuring.

In 2020, with the enactment of the CIGA, many of the features found in Chapter 11 are incorporated in the UK’s restructuring regime. These include a standalone moratorium in order to effect a restructuring45 and a cross-class cram-down.46 In the former, it provides the company with an initial breathing space of 20 business days and the directors may file for an extension of a further 20 business days. Any extension beyond 40 business days requires the consent of the company’s pre-moratorium creditors or the court. Under the restructuring plan introduced by CIGA, with the sanction of the court, it is possible to effect a cram-down across classes of creditors. The CIGA restricts the use of ipso facto clauses in contracts for not only the essential supply provisions that were previously found in the Insolvency Act 198647 but also the contracts for the supply of goods and services, though there are exemptions.48 When a company becomes subject to a relevant insolvency procedure, including the statutory moratorium, administration and restructuring plan (but not the scheme of arrangement), the provisions apply to any clause in a contract for goods or services that automatically terminates the contract or entitles the supplier to terminate the contract upon the company being subject to an insolvency procedure. However, there is no wider ban on ipso facto clauses of the width that is found in Chapter 11.

Finally, there is administration. The objectives of administration stated in the legislation are: (1) to rescue the company as a going concern; (2) to achieve a better result for the company’s creditors as a whole than would be likely if the company was wound up; or (3) to realise the company’s property in order to distribute to its secured or preferential creditors.49

Once the company is put into administration, the administrator, who is a qualified insolvency practitioner, displaces the board of directors, has the powers to manage the business affairs of the company, and presents the plan (that will achieve at least one of the above-mentioned objectives) for the creditors to approve. While the English administration is a PIP regime (since the directors are displaced in favour of the insolvency practitioner), developments since the onset of COVID-19 pandemic show that the market practitioners are using a ‘light touch’ administration, where the administrator allows the management to exercise some of these powers while the administrator continues to have oversight.50

1.2.3.Transplanting US/UK Restructuring Concepts in Asia

The four Asian jurisdictions under study have all adopted restructuring regimes based on US and/or UK models. Hong Kong’s scheme of arrangement draws on the UK case law on English schemes, being a secured creditor-in-control model, though Hong Kong may be moving ahead with a corporate rescue mechanism.51 Under a secured creditor-in-control model, no restructuring is possible without the consent of the secured creditors. It is not possible to effect a cross-class cram-down in Hong Kong or (prior to 2017) Singapore due to the absence of an equivalent UK process which allows for administration that is twinned with schemes of arrangement.52 In the case of Singapore, in fact, prior to the enactment of the amendments to the company legislation and insolvency law framework in 2017, its regime was a distinctly secured creditor-in-control model that was similar to Hong Kong. Since these reforms, Singapore’s scheme of arrangement has shifted distinctly to a DIP model that is based on Chapter 11.53

There are currently three main gateways to restructuring in India: (1) via the Indian Insolvency and Bankruptcy Code 2016; (2) the scheme of arrangement under the Companies Act 2013,54 and (3) Reserve Bank of India’s 7 June 2019 circular on the Prudential Framework for Resolution of Stressed Assets, which is an out-of-court mechanism for banks’ resolution of stressed assets involving large accounts.55 Gateways (1) and (3) are used regularly in India. Gateway (2) is seldom used as a tool of debt restructuring in India due to the inefficiencies of the court system.56 Gateway (3) is a mechanism for an out-of-court bank-led creditor restructuring, which is often used by RBI-regulated entities to resolve non-performing assets (NPAs) and take advantage of the prudential norms applicable for NPAs following restructurings where the borrowers have aggregate exposure of Rs 15 billion (USD$202 million).57 The IBC, introduced in 2016, is by far the most significant piece of restructuring legislation. Its model is that the insolvency practitioner, known as the resolution professional, takes control of the assets, similar to the PIP model found in the UK’s administration proceedings under the Enterprise Act 2002.58 The IBC will be the focus of discussion in this book.

In Mainland China, the only method for corporate restructuring is prescribed under the Enterprise Bankruptcy Law 2006 (EBL), which became effective on 1 June 2007, as well as the judicial interpretations and notices issued by the Supreme People’s Court (SPC) and the typical case lists that are issued by the SPC.59 The EBL is the most significant piece of modern restructuring law in an emerging jurisdiction, and its inspiration was drawn from Chapter 11 of the US Bankruptcy Code 1978, the UK, Germany and Japan.60

The EBL is a hybrid of the DIP and PIP model where either the debtor or the administrator can propose the plan.61 The debtor can continue to manage the business and operations whilst in reorganisation, with the approval of the court, whilst the administrator supervises the process.62

1.3.UNDERSTANDING THE INTERACTION BETWEEN CORPORATE GOVERNANCE AND RESTRUCTURING LAW

Given the goal of restructuring law is to minimise the costs of restructurings of financially distressed but otherwise viable companies, the key question is how to manage frictions among the stakeholders. There is a rich body of literature as to agency costs; in corporate governance literature, where the shareholdings have been dispersed, the key question is managing the agency costs relating to the conflicts between the shareholders and management. The most influential analysis was conducted by Jensen and Meckling,63 who demonstrated that while the firm raises outside capital, it benefits from economies of scale. However, at the same time, agency costs arise because managers have an incentive to engage in conduct, such as shirking or taking, that benefits them personally, though such behaviour is value-destructive.64 Debt is an important factor to mitigate these costs as debt limits the discretion of management in engaging in wasteful projects.65 As long as the firm is solvent, the management will be kept in check; the creditor’s standard contractual right against the firm to sue for repayment (with eventual liquidation if repayment is not made) is presumed to incentivise the debtor’s manager to keep the company solvent.

In corporate governance literature on Asian firms where the shareholdings are concentrated in the hands of families or the state, the focus is on managing the agency costs between the controlling and minority shareholders.66 The managers are appointed by the controlling shareholders and hence would be expected to be aligned to the interests of the controlling shareholders.

However, in either situation of controlled or dispersed ownership, once the company enters into financial distress (whether through fraud, managerial incompetence or unfortunate circumstances), the interests of shareholders and creditors diverge sharply. The shareholders are keen to gamble for resurrection and engage in risky projects, when creditors are interested only in getting repaid. Even if ownership is dispersed, it would be expected that management will side with shareholders since they may lose their jobs when the company goes into insolvent liquidation. Creditors may also engage in grabbing the assets of the debtor first, even if all of the creditors and other stakeholders would have been better off overall if the company remains economically viable and can benefit from restructuring. Insofar as creditor–creditor relationships are concerned, agency costs arise where the interests of the majority of the creditors (the agent) diverge from the minority of the creditors (the principal) or where the interests of one class of creditors diverge from the other classes. As the number of creditors increase, there will also be an increase in the costs of coordination.

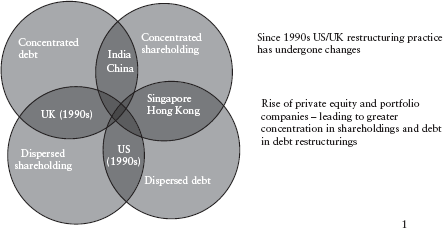

While there is a rich body of literature discussing the trade-offs and optimal design of restructuring law and policy in addressing agency costs of creditor-shareholder, creditor-management and agency and coordination costs of creditor–creditor relationships, the literature is largely located in the US/UK. For example, in an influential paper, Skeel argues that the debtor in possession (DIP) or ‘manager in control’ model of Chapter 11 is complementary and is co-related to a dispersed ownership.67 Nuance was added in a follow-up work by Armour, Skeel and Cheffins: the US model is both co-related to dispersed ownership and widely held debt, while the UK model of ‘manager displacing’ or creditor-driven bankruptcy regulation is co-related to its dispersed shareholding ownership but concentrated debt structure.68 Since this work, the English scheme of arrangements have been widely used as early modes of restructurings. The English scheme may be twinned with administration under the Enterprise Act 2002, which displaces the managers in favour of the insolvency practitioner.

Figure 1.1 shows the interaction between shareholders and creditors in the Anglo-American and Asian frameworks.

Figure 1.1Interaction between shareholders and creditors in Anglo-American and Asian frameworks

After the publication of Skeel and his co-authors, the capital markets in the US and the UK underwent significant changes beginning from 2000. Private equity sponsors become very active in engaging in takeovers of publicly listed companies and subsequently taking them private or acquiring other privately held companies.69 The shareholding structures of these firms, ie portfolio companies, become concentrated after the buy-outs, and the deals are highly leveraged, financed with a mix of equity and junior debt provided by the private equity sponsors and senior debt arranged by bank lenders.70 Management is also often given incentive in the form of equity to align their interests with the private equity funds. The investment horizon is limited in time (three to seven years), and the aim of the investment is to re-list the company in a stock exchange or undertake a trade sale.71 During the global financial crisis of 2008, these highly leveraged portfolio companies became susceptible to financial distress and had to be restructured.72 At the same time, changes to the US Uniform Commercial Code in 2001 had improved the position of the secured creditor to take security over the whole of the assets of the company.

Paterson argues that there is some convergence between the US and UK models due to the presence of adaptive devices in both jurisdictions and certain other factors, including the increasing power of secured creditors in Chapter 11 proceedings and the rise of high-yield debt in the UK.73 Further, finance scholars have pointed out that the debt in Chapter 11 restructurings may not be static; it could be widely held at the time of filing but becomes more concentrated as a result of distressed debt investors purchasing debt prior to the voting on the plan.74 Most recently, the UK has introduced a new flexible restructuring process in CIGA, which is based on Chapter 11.

Influential as these theories are, it is doubtful if they can be applied to the restructuring of Asian companies. First, the theories by Skeel and his co-authors do not capture the interaction between corporate governance and bankruptcy/insolvency of financially distressed firms where the shareholders are concentrated, given that they dealt with Anglo-American firms in the 1990s. Since 2000, Anglo-American scholarship documents the changes in bankruptcy practice and, in particular, the increase in concentration in shareholdings in private equity portfolio as a result of the leveraged buy-outs occurring. However, much of the scholarship continues to be located in the US and UK, and in the case of the US, the emphasis is on sidelining the shareholders when the company is in financial distress. In this work, I explain how and why shareholders (being families or the state) have influenced the outcomes of restructurings of large companies and their associated transaction costs in the four Asian jurisdictions. For instance, even if assets are worth less than the debt, one may be in favour of by-passing the intermediate classes of junior creditors and award some of the distributions to old shareholders who may bring in new capital but will baulk if the old shareholders have been dishonest or are otherwise perceived to have contributed to the company’s financial distress.

Second, as will be explained in this book, the debt that is sought to be compromised under restructuring in Asian companies is not identical to the debts that are sought to be compromised in the US and UK restructurings, and this debt has also been subject to changes in recent years. Even between the US and UK, there are differences. In the US, Chapter 11 restructures the whole balance sheet of the company, including the financial debt, operational debt and unpaid workers’ wages. English schemes and pre-packaged administration plans are traditionally concerned with financial restructuring only and the company continues with its existing suppliers.

Mainland China is the closest to Chapter 11 in terms of restructuring both financial and operational debt. However, while, prior to 2015, the debt was still primarily bank debt for which restructuring was sought, the situation has since undergone significant changes as bond issuances have ramped up significantly. Post-2015, more companies have raised debt financing in the public markets and more companies have defaulted on their bonds.75 The creditors thus are much more diverse and include bondholders. Likewise, in India, onshore bond issuances have risen since 2010, and there is also an active market for distressed loans given that India is an emerging jurisdiction where it is possible for distressed investors to turn many of the distressed assets around for profits.76

In Singapore and Hong Kong, which have English-modelled schemes of arrangement, the debt that is sought to be compromised does not comprise only financial debt but also operational debt held by a number of trade creditors. Even among the financial creditors, there is no uniformity as they may include not only banks but also non-institutional creditors (such as retail bondholders). In India, the negotiation process under the Indian IBC only comprises the financial creditors; however, as can be seen from later chapters, financial creditors may also include the diverse group of home buyers in real estate development insolvencies.

Therefore, the rules governing the bargaining process by the stakeholders (creditors, shareholders and management) in Anglo-American restructurings may not be suitable for Asian restructurings where there are many (and different) conflicted parties. Yet, these rules are essential as they tell us how these negotiations are conducted (for example, through creditor committees or classes of creditors) and whose consent is required to negotiate to compromise the claims, in order for the bargaining process to be efficient and reduce transaction costs.

Third, with some rare exceptions, notably during the global financial crisis for the rescue of what are deemed systematically important companies, the literature on US77 and UK restructuring in these strong market economies assumes that the creditors want to maximise the value of their assets in the bankruptcy outcomes, though there may be differences in views as to how maximisation should take place. Further, the assumption is that bankruptcy proceedings are not the sole debt collection devices for creditors; if restructuring fails, the creditors will enforce their rights elsewhere in the courts and ultimately put the companies into insolvent liquidation, though such enforcement may be less effective in achieving the desired recovery.78 Both assumptions cannot always be relied on in emerging jurisdictions where the state is also a creditor and/or shareholder. In particular, in Mainland China and India where non-performing loans are a perennial problem in the banking sectors, mechanisms such as asset management companies (AMCs) are used to purchase these loans, which have an impact on agency and coordination costs as the AMCs serve as the new creditor in place of the lender. In the case of India, enforcement via the courts is often hampered by delays, making the Indian IBC the preferred (and often only) choice in recovery, and thereby creating pressures on the judicial systems administering the Indian IBC.

While scholars have engaged with comparative insolvency law between the US and the UK,79 save for certain exceptions,80 there is a dearth of academic literature on optimal design of restructuring framework in Asia that takes into account the relationship between corporate governance and restructuring law and practice. This book aims to fill the gap in the literature on legal transplantation as applied to restructuring of financially distressed companies.

1.4.BUILDING AN ANALYTICAL FRAMEWORK

The luxury of the space afforded by this book allows an investigation on how agency conflicts arise and are resolved in Asian jurisdictions. The comparison is not made in a vacuum and takes place in a framework of established scholarship on agency and coordination costs in the US and UK, but with key institutional differences. The choice of jurisdictions is explained below.81

The central thesis of this book is that an optimal design must take into account the following that are absent or not present to the same extent as in the US/UK: (1) the interaction between concentrated shareholdings and widely held debt leading to significant risks of prejudice to outside creditors; (2) the incentives of the state in resolving non-performing loans for the purposes of bank regulation; (3) the benefits and limitations of the independent gatekeepers, being the insolvency practitioners and the courts; and (4) the interaction among restructuring law and enforcing contracts and duties of directors of financially distressed companies.

It is not the purpose of this book to weigh in on the debate on the wider question on whether the goals of restructuring law should be confined only to the economic outcomes (as encapsulated by the Creditors’ Bargain theory) or should be progressive in using restructuring law as a tool to promote reorganisation.82 This has been ably done by other scholars.83 Rather, the book has taken the normative Creditors’ Bargain theory as the starting point that the goal of restructuring law is to minimise transaction costs ex post the commencement of the restructuring process and up to the time of exit. The book assumes that even if a progressive approach is taken towards reorganisation, it must be the goal to minimise transaction costs.

These issues will be even more relevant today as each jurisdiction is expected to deal with the rise of restructuring filings due to the economic fallout from COVID-19.

1.4.1.Management–Creditor and Shareholder–Creditor Conflicts

The aim of the DIP regime is to allow the management to drive the restructuring. In Anglo-American restructurings, shareholders of a distressed company are treated as having no economic interests of the company. In particular, where the company has dispersed shareholdings, and shareholders do not operate the firm but entrust the operations to professional managers, managers in any event are likely to pay more attention to creditors. The exception is where the management of the company is perceived as having brought about the distressed situation through fraud or incompetence. Even in the case of portfolio companies where the shareholdings are concentrated in the hands of private equity firms, the decisions will continue to be made based on market-oriented outcomes.

Controlling shareholders are dominant in Asian economies, in contrast to the dispersed shareholding structure found in the publicly listed companies in the US and the UK. Conventional US/UK scholarship has argued that concentrated shareholding is generally detrimental for corporate governance and the conversations have shifted to policing the private benefits of control between the companies and controlling shareholders. Many scholars have also argued that concentrated shareholdings are not appropriate for DIP models which may serve to entrench existing management, which led the company into financial difficulties in the first place.84

However, simply rejecting the DIP framework for jurisdictions with controlling shareholders is often not optimal since they are important in determining the outcomes of successful restructurings. Further, the absolute priority rule (APR), a cornerstone of the US Bankruptcy Code which allows the court to exercise cram-down of dissenting classes of creditors only if, among others, senior creditors must be paid in full before junior creditors or shareholders can receive anything, is not necessarily optimal if the interests of shareholders (including controlling shareholders) are to be wiped out after the restructuring.

Thus, the regime should incentivise controlling shareholders to participate if they are able to add value. However, the conflicts of interests posed by controlling shareholders need to be addressed, including controlling their participation in the outcomes, mandating disclosures of the debtor’s financial information (and in early in the process), and addressing gaps in the enforcement of directors’ duties.

1.4.2.Creditor–Creditor Conflicts

Until the 1990s, restructuring in the UK took place largely in the context of financial debt held by banks. Even with the rise of private equity portfolios after 2000, schemes of arrangement and pre-packaged administration plans were traditionally used to reorganise financial debt only. Only recently has there been a shift towards the reorganisation of operational debt, particularly under Part 26A. In contrast to the UK, Chapter 11 involves the restructuring of the whole of the balance sheet of the company and the debt has traditionally been more diverse than in the UK. In both the UK and the US, the developments in the markets, including the rise in leveraged debt financing and distressed debt trading, has weakened the dominating power of the banks.

The debt markets in the four Asian jurisdictions have also experienced increases in complexity in the last two decades. Until the late 1990s, Mainland China and India have concentrated debt markets dominated by bank lending. As chapter four demonstrates, bond issuances have increased dramatically since 2000, and it follows that onshore bond defaults become more prominent. In Mainland China, onshore bonds are often widely held across institutional and non-institutional holders. Partly to address concerns as to social unrest, the restructuring regime has resulted in departures from equal treatment of the same class of creditors, such as between smaller and larger bondholders.85 Likewise, partly to address concerns of social unrest, different treatment also occurs between financial and non-financial creditors even among the same class. In India, while all of the creditors will be bound by the corporate resolution process under the IBC, the resolution process involves voting by financial creditors and not operational creditors as the latter could be extremely numerous and it is extremely time-consuming to coordinate the process.86

Even though Singapore and Hong Kong draw their schemes of arrangement framework from UK, the composition of the debt-holdings of large companies has some similarities but also key differences. In Singapore and Hong Kong, trade creditors routinely have their debts compromised. Further, bond debt in these two Asian markets is widely held by not only institutional creditors but also non-institutional investors (such as individual or retail investors) due to the several regulatory policies that encouraged non-institutional investment in corporate debt.

In addition, the creditors that are present in Asian restructurings often present risks of the scale that are not necessarily present in the US and the UK. Creditors in Asian restructurings are often related parties and face conflicts of interests because they or their affiliates are shareholders or are shareholders of affiliated companies. These creditors would also be privy to information that is not available to other outside creditors, and the debtor’s management often have no incentives to disclose information (or to disclose information early) to the creditors in the absence of mandatory requirements.

1.4.3.Non-Performing Loans Management

If a creditor bank participates in a restructuring process, it would generally be expected that it would be motivated by market reasons to maximise its recovery. However, if a bank is not in good financial health due to its non-performing loans (NPLs), it may prefer to postpone the restructuring or may refuse to accept a haircut but take a longer tenure for the loan. How the banking regulator encourages speedy resolution of NPLs will affect the incentives of the bank creditors in participating in any restructuring.

However, where a jurisdiction’s NPLs are unacceptably high, banking regulators have to intervene to ensure the stability of the country’s banking market; high levels of NPLs depress credit growth, impede recovery and do not allow assets to be put to productive use.87 In dealing with NPLs, it is well established that reforms to the insolvency and restructuring law framework for such NPL resolution is important.88 However, it is also clear that insolvency law reforms are not, by themselves, the complete cure. Certainly, banking crises in the last three decades, including the savings and loans crisis in the US in the 1980s, the Asian financial crisis in 1997 and the global financial crisis in 2008, reveal that advanced and emerging jurisdictions will have to use other measures, including a series of bank regulatory measures (such as less favourable bank provisioning for NPLs and off-loading of the NPLs), bank bail-outs or bail-ins, tax measures and accounting rules.89 In the bank regulatory measures to off-load the NPLs, two are prominent: using asset management companies (AMCs) or their equivalents to acquire the NPLs and thus taking the NPLs off the balance sheet of the banks; and increasing external investor participation in the secondary market for NPLs.

The analysis of the standard agency and transaction costs in restructuring proceedings must consider further the use of asset management companies and the consequences of opening up the market to distressed trading. AMCs and distressed debt market can reduce the agency and transaction costs in at least two ways. First, by mandating the banks to sell the NPLs only to the AMCs in the primary market, the AMCs can more easily aggregate debt and potentially reach faster resolutions for the NPLs. Second, the relationship between the lender and the debtor changes as the new lender has acquired the NPLs (usually at a discount). If the reason for the NPL problem is that the banks are not sufficiently disciplined to clean up the NPLs, AMCs (or the subsequent secondary purchasers of the NPLs) should instil the discipline in maximising recoveries, particularly if NPLs are acquired on market terms and these purchasers have to account to their own stakeholders.

In Mainland China, the national and provincial asset management companies, which are formed to take over the NPLs are largely state-owned. In the case of India, the equivalent counterpart are asset reconstruction companies though there is a higher degree of foreign or private ownership. The distressed loan market in India is particularly vibrant in view of the fact that it is an emerging economy (which means that there is great potential for certain assets to be turned around). The enactment of the IBC which allows the creditors a clearer path of recovery has certainly been very helpful.90 Using asset management companies or their equivalents lead to an important change in the way the agency and coordination costs are played out in the restructuring as they purchase the NPLs and take the place of the original lender. However, state-owned asset management companies may face the same incentives as state-owned banks in their reluctance to resolve NPLs and adopt non-efficiency-based solutions. As jurisdictions seek to promote foreign investors to invest in asset management companies, purchase NPLs and/or create active distressed markets, it is even more critical to identify the agency and coordination costs that are posed by these companies.

The successes of the US Chapter 11 and English scheme have been credited in significant part to the presence of the effective judiciary and the bankruptcy professionals. Law and economics scholars have argued that the jurisdictions with poor legal development and lacking in judicial expertise are better off with a more creditor-friendly regime.91 The difficulties faced by Mainland China and India in their paths towards insolvency reforms have been attributed to, among others, the absence of the judicial expertise in handling commercial insolvencies (eg Li and Ponticelli92 (China), and van Zwieten93 (India)).94 However, while an effective and competent judiciary and a highly developed profession of insolvency practitioners are important, they are not in themselves sufficient to ensure effective oversight and thus the success of the restructurings in Asia.

There are limitations to relying only on the courts and insolvency practitioners to enforce a transparent and consistent restructuring regime. The development of these mechanisms will take time and often even well-trained judges are often not in a position to decide who is acting opportunistically, nor can they assess proposals that are not even put on the table. Insolvency practitioners often face conflicts of interests and where enforcement of underlying contracts is unclear, administrators are not in the best position to determine the admission of claims for the purpose of voting.

1.4.5.Non-Bankruptcy Rules on Enforcing Contracts and Directors’ Duties

It is well established in the literature that an assessment of a country’s creditor protection depends on the efficacy of both the ability of the creditor to enforce their rights (and either liquidate the company or take possession of their security) as well as its powers to influence the outcome of the reorganisation.95 In the Anglo-American view of bankruptcy law, where restructuring fails, the creditors have alternative remedies in enforcing their debts in the courts, putting forth their claims in liquidation and repossessing the collateral. Thus, in analysing the shareholder–creditor, management–creditor or shareholder–creditor agency and coordination costs, the only concern will be in respect of the restructuring process.

However, in emerging jurisdictions, enforcement of unsecured debt may be weak, and liquidation takes a long time. Secured creditors may also not be able to repossess the collateral readily without obtaining court orders or jumping through other hoops (while continuing to have the power to vote to influence the outcome of the restructuring). In these cases when the alternative of recovery though enforcement or liquidation is not readily available, the agency costs of shareholder–creditor and agency and coordination costs of creditor–creditor relationships will be exacerbated. If creditors realistically only have the option of invoking the restructuring process in an attempt to receive their claims, the regime will be extremely protective of the debtor unless the restructuring process is efficient. For instance, in India, prior to the IBC, the non-bank unsecured creditors had little prospect of recovery of their claims through the courts and secured creditors faced many obstacles in repossessing the collateral. Thus, the regime was too friendly to the debtor (and its management and controlling shareholders). The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act 2002 (SARFAESI) facilitated out of court enforcement by secured creditors but only for the financial institutions. If repossession of the collateral is difficult or challenging, the secured creditors in effect receive less protection (vis-a-vis the unsecured creditors and managers) and the effect is similar to that of an automatic stay on the assets against the secured creditors outside the restructuring process. These conceptual difficulties arise when analysing the appropriate reforms.

Further, how effectively the jurisdiction enforces directors’ duties also impacts on when the directors invoke the insolvency or restructuring framework. If directors’ duties are well enforced and there are adverse consequences for the directors if they continue to allow the insolvent company to continue trading, the likelihood is that such they will seek assistance early and the more likely it is that the company can be rescued, leading to savings in transaction costs.

1.5.1.Distinction between Deployment and Distribution

In analysing the agency and coordination costs in this book, I deal with the questions as to deployment (how the assets should be used) and distribution (how much creditors will receive) separately. This distinction is grounded from a long line of corporate finance literature, including a seminar paper by Modigliani and Miller96 which established that the market value of a firm depends on its underlying assets and the present value of future cash flows and is thus independent of its capital structure. Using Modigliani and Miller’s theory and extrapolating in the bankruptcy context, how the assets should be deployed and who has rights to those assets are separate questions.97

While Chapter 11 requires the creditors to bargain as to both deployment and distribution in the reorganisation process, this is not necessary the norm even in advanced economies. For example, in a PIP model in the UK administration proceedings (see Table 1.1), the process does not require the creditors to bargain over distribution and the question of deployment is carried out by the administrator.98 The administrator has the power of sale of assets, and is able to leave behind the liabilities, and thus only negotiates the sale with the intended new purchaser in a pre-pack sale. The distribution of the proceeds of sale will follow the priority rules that apply in the case of liquidation.

1.5.2.Court Restructurings of Large Companies

In this book, I focus only on court restructurings and exclude, for example, UK company voluntary arrangements (which do not require the supervision of the courts).99 Administration is included in the discussion, particularly in chapter six on the role of the insolvency proceedings since administration can be granted by the court,100 corporate rescue is one of the possible outcomes of administration.

There are a number of reasons for focusing only on court proceedings. First, in the four Asian jurisdictions (see Table 1.1), excluding out-of-court workouts which are often difficult to study empirically due to the lack of data, the court-supervised restructuring remains the dominant mode of restructuring in comparison with the PIP models. Singapore is an exception as it is possible to effect an out-of-court judicial management.101 Second, whilst many reorganisations take place consensually, bargaining ultimately takes place in the shadow of the law, which influences the outcomes of these bargains.102

Due to both space constraints and the availability of data (such as restructuring plans and related documents), I have only focused on large company restructurings in the four Asian jurisdictions. For the discussion on Indian restructuring, I have focused only on the IBC (as opposed to the schemes of arrangement because schemes are not widely used for debt restructurings).103 I have excluded small and medium enterprise restructurings, which are increasingly subject to a different restructuring framework, as is the case in India104 and Singapore.105

1.5.3.Choice of Asian Jurisdictions

I study Mainland China, India, Hong Kong and Singapore for the following reasons.

First, they are located in Asia and represent a mix of debt resolution in two economically advanced (Singapore and Hong Kong) and two emerging (Mainland China and India) jurisdictions. Mainland China and India are the second and fifth largest economies in the world, measured by GDP. Second, all four economies have listed companies that have concentrated shareholdings and vibrant capital markets whose companies regularly issue public debt.

Third, the four jurisdictions have explicitly drawn attention to the fact that they have transplanted restructuring models from UK/US, though there are differences. Mainland China enacted the Enterprise Bankruptcy Law (EBL) in 2006, which borrows from, among others, US Chapter 11, the UK administration and the German Insolvency Code of 1999, as well as the recommendations of the UNCITRAL Legislative Guide on Insolvency Law 2005.106 Singapore amended its schemes of arrangement (originally based on the English schemes), drawing the features inspired from Chapter 11, and whose provisions are now found in the Insolvency, Restructuring and Dissolution Act 2018 (IRDA). India enacted the IBC in response to its NPL problems, and the solutions that India seeks are similar to the practitioner in possession (PIP) model found in the UK’s administration proceedings. After almost two decades of consultation, Hong Kong (whose framework is based on English schemes) may be moving ahead with bankruptcy reforms which are likely to include a corporate rescue regime.107 Currently, Hong Kong’s regime is based on English schemes and with significant rights retained by secured creditors in vetoing the restructuring.

Further, this book will explain how the experiences of the four jurisdictions are relevant to one another and how these lessons may be generalised in relation to other jurisdictions.

There is no question that Mainland China is firmly moving towards market-driven restructuring,108 even though there are some accounts of Chinese bankruptcy practice focusing on governmental influence in bankruptcy process and the lack of institutional support in the restructuring process.109 Ministries have issued notices for the clean-up of ‘zombie companies’ using market-based methods.110 More recent scholarship also points out its remarkable progress towards market-based bankruptcy system and institutional capacity-building.111 By early 2020, mounting levels of distressed debt, due to the slowdown in the economy and the trade war with the US, had led to NPLs in Mainland China exceeding US$1.5 trillion.112 While China’s asset management companies (AMCs) were set up to purchase the NPLs from the state-owned banks since 1999, the NPL market is opening up to foreign investors in order to clean up the bad debt problem. Phase one of the trade deal between the US and China (the Economic and Trade Agreement) allows for US financial services firms to apply for licences to set up AMCs. Foreign investors would expect predictability and transparency in the treatment of the distressed debts in the courts, whether through enforcement or bankruptcy,113 and the recent experiences of China on resolving NPLs through insolvency law will be relevant for other emerging jurisdictions that are transitioning into market-based restructurings and facing high levels of NPLs.

In India, the Sick Industrial Companies (Special Provisions) Act 1985 was introduced, which by most accounts was a failure.114 Later attempts, such as the Recovery of Debts due to Banks and Financial Institutions Act 1993 and SARFAESI, are only applicable to banks and financial institutions. In 2016, the Insolvency and Bankruptcy Code (IBC) was introduced, which laid down a time-bound insolvency procedure for companies to be resolved. The IBC has been transformational, both in moving the regime from a strong debtor-friendly regime to one that is creditor-friendly, and one that is led by insolvency practitioners as opposed to being controlled by debtors. The IBC is also an important tool to resolve some of the NPLs. How the distressed debts in the NPL market are dealt with in the courts (whether under the IBC or in enforcing contracts under general law) will be critical in the strategy towards moving to a more market-based restructuring. The experience of India will be relevant to other emerging jurisdictions as to how insolvency law reform can dramatically impact the shift between a debtor-friendly to creditor-friendly regime.

Singapore’s rationale for adopting Chapter 11 in its schemes framework was different from the other three jurisdictions: it was motivated by becoming a regional restructuring hub.115 However, Singapore’s debt market has significant retail investment, due to the institutional factors in encouraging the development of an active retail market for corporate bonds. The experiences of Singapore on Chapter 11-style restructurings in the context of concentrated shareholding structure and dispersed debt-holding demonstrates the lessons that can be learnt in jurisdictions with both concentrated shareholding and dispersed debt-holding. Its experiences on judicial management (which has some parallels with the administration process in the UK) will also be useful to jurisdictions considering the PIP model.

Hong Kong’s restructuring law is largely based on the traditional English schemes of arrangement. The Hong Kong Government is proposing to enact legislative reforms to allow for provisional supervision and corporate rescue, which are out-of-court procedures, to facilitate restructuring if the major secured creditor consents.116 As with Singapore, the lessons of Hong Kong in effecting schemes of arrangement of companies with concentrated shareholding structures and dispersed debt-holdings offers lessons for other jurisdictions. Hong Kong’s experience with soft-touch liquidation (explained in the next section) also holds lessons of the future of a DIP regime.

In relation to the materials on Chinese bankruptcy law, I refer, where possible, to the English sources. Where the original sources are only available in the Chinese language, I include the Chinese language references as well to facilitate Chinese-speaking readers to locate the sources. I have included a bilingual list of judicial and policy guiding documents for readers so that Chinese language readers can refer to the original sources, since many of them do not have official English translations.

1.5.4.1.Theoretical and Comparative Framework

In the theoretical framework, the study engages with the theories of Skeel, Armour and Cheffins, as well as Skeel, Baird and Rasmussen, Skeel and Triantis, and Paterson, who consider the later developments in the debt markets,117 and who seek to explain the UK and US bankruptcy models on the basis of shareholding dispersion and different debt structures. The book tests whether these theories can be extended to Asia, by looking at the inefficiencies that arise due to shareholder–creditor, shareholder–manager, and creditor–creditor conflicts, the banking regulator’s management of the NPLs, and the efficiency of the institutional structures.

In this book, the DIP model under study is Singapore’s schemes of arrangement post-2017 reforms; a hybrid form of DIP and PIP models is Mainland China’s EBL, and the PIP models in the Indian IBC and Singapore’s judicial management.

Mainland China is classified as a hybrid form of DIP and PIP because while certain aspects of the EBL is modelled after DIP in Chapter 11, once the debtor enters into reorganisation proceedings, the court-appointed administrator directly manages the property and affairs of the debtor. However, the debtor can apply for its management to be in control but under the supervision of the administrator.118 The latter will require court approval.119 Either the debtor or the administrator is responsible for formulating the reorganisation plan, depending on which one manages the business.

Hong Kong utilises the English-origin schemes of arrangement to restructure both financial and operational debt, which I have classified as ‘secured creditor-in-control’, given that any scheme can only proceed with the consent of the secured creditors. As there is no free-standing automatic stay on enforcement proceedings, prior to Re Legend International Resorts Ltd,120 a decision of the Hong Kong Court of Appeal, the market has used provisional liquidation (which allows for automatic stay of proceedings) to facilitate corporate rescues via schemes of arrangement. However, in Re Legend, by way of dicta, the Court of Appeal held that provisional liquidation cannot be used to effect a corporate rescue. This created uncertainty as to the use of schemes of arrangement for corporate rescue since the Hong Kong scheme does not carry with it a moratorium. Eleven years later, in a series of judgments arising from Re China Solar Energy Holdings Ltd,121 the Court clarified that the limitation in provisional liquidation does not preclude its use when the assets are in jeopardy. However, it should be noted that provisional liquidation does not stay enforcement of secured debt but only the unsecured debt.

There is a further layer of complexity in Hong Kong, which is the use of the soft-touch provisional liquidation. Almost 80 per cent of the listed companies in Hong Kong are incorporated outside Hong Kong, notably in the Cayman Islands, the British Virgin Islands and Bermuda.122 In recent years, debtors have gone to these jurisdictions (being the place of their incorporation) to appoint provisional liquidators for the purpose of restructuring, though such appointment is not allowed in Hong Kong. Unlike provisional liquidation in Hong Kong, the appointment of soft-touch provisional liquidators does not displace the directors. Debtors have then proceeded to seek a recognition of such appointment in Hong Kong.123 For reasons explained in chapters two and four, including the fact that the courts are cognisant that debtors may have abused the process in seeking soft-touch liquidation to delay proceedings as opposed to genuinely attempt restructuring, the impact of such recognition in staying winding-up proceedings to effect a restructuring is now becoming very unlikely.

Banking regulation has had a large impact on the development and impetus on the development of restructuring law in Mainland China and India. Mainland China and India have contributed to the largest NPL portfolio in Asia (collectively amounting to 75 per cent).124 One key solution adopted by these jurisdictions is to set up AMCs to ringfence the non-performing assets and allow for these assets to be disposed or restructured. Existing literature has highlighted the potential advantages of the AMCs over other market-based solutions including the economies of scale in workouts, the granting of special powers to the AMCs to deal with loan resolution and having a disinterested third party to mediate between the bank creditor and the debtor.125 However, as many of the AMCs in Mainland China are still state-owned, they have been criticised as lacking incentives to effectively restructure the NPLs that they have acquired from the state-owned banks.126 But with China and India127 opening up their economies by allowing greater participation in the AMCs by foreign investors, this book will address the changing incentives of AMCs.

Finally, the book will address the effectiveness of the institutional structures in place to support restructuring law, such as the judiciary and insolvency profession. The ease in which debts are enforced and how directors’ duties are enforced are also addressed.

Due to limitations of space, I make certain omissions. First, I will not be covering the cultural factors behind the motivations of the Asian entrepreneurs in using credit and invoking insolvency and restructuring laws as compared with the US/UK, including whether there are differences in the perceptions of bankruptcy stigma. Readers will be advised to look at the literature discussing cross-cultural differences in their attitudes towards risk-taking.128 Second, as the book focuses primarily on institutional structures and the framework, I exclude the broader discussion on the political environment that may have influenced the choice of insolvency and restructuring law. Instead, the book will focus on the role of the state as a shareholder (particularly in the case of Mainland China), in the context of its highly visible roles in listed company and international bond restructurings. Third, as mentioned earlier in this chapter, the book is concerned with primarily ex post transaction costs when the company is in financial distress. Thus, the book will not go into detailed treatment as to how legal traditions and origins impact the choice of insolvency and restructuring law. Fourth, I have mainly concentrated on the domestic insolvency and restructuring framework in the jurisdictions and have not discussed cross-border elements of restructuring in the four jurisdictions, except in the context of Hong Kong and Mainland China, due to the fact that many large restructurings in recent years involve cross-border restructuring practice, and the practice has a substantial impact on the development of the jurisprudence in insolvency and restructuring law. Fifth, I have excluded discussions of restructuring of financially distressed financial institutions and banks as they are subject to specific bank resolution regulation. Sixth, the book is only concerned with corporate restructuring law, and not personal bankruptcy law.

1.5.4.2.Empirical Studies

In the empirical studies of the four jurisdictions, I examine the outcomes of the restructuring and analyse the outcomes using the framework set out above on resolving shareholder-creditor, shareholder-manager and creditor-creditor conflicts. With certain exceptions on Mainland China,129 India130 Hong Kong131 and Singapore,132 there are few empirical studies on the impact of the restructuring laws on creditor and shareholder outcomes as well as the impact of NPL regulation on restructuring law.

The main empirical sources of data for this book are set out below.

1.5.4.2.1.Mainland China

For Mainland China, my approach will build on prior studies which have focused that the outcomes of listed company restructurings are attributable to governmental intervention.133 I have extended the dataset substantially to include companies that issued public debt. Thus, the dataset comprises the outcomes of the reorganisation of large companies (which will be the companies that issued public debt (in Panel A of Appendix A) and listed companies (in Panel B of Appendix A). The period under investigation will be 2015–19. 2015 is chosen as it is the year in which the Communist Party of People’s Republic of China identified improving the implementation of EBL as one of its key priorities, given EBL’s importance as a market-based mechanism to resolve insolvent companies.134 Data will be the judgments and restructuring plans obtained through National Enterprise Bankruptcy Information Disclosure Platform (‘Platform’)135 that was launched in August 2016 by the Chinese Supreme People’s Court (SPC), which allows for the debtor companies and creditors to monitor the development of the cases,136 as well as from WIND database, a subscription database and press articles. For the status of bond restructurings, I refer to Fitch Blue Book, which provides the status of bonds in default137 and cross-checked with WIND database, which contains the announcements by the companies whose bonds are in default.

Data on the NPLs acquired by AMCs in China will be drawn from the public disclosures by the four national AMCs, comprising China Huarong Asset Management Co Ltd (Huarong), China Cinda Asset Management Co Ltd (Cinda), China Orient Asset Management Company Limited (China Orient) and China Great Wall Asset Management (Great Wall). Huarong and Cinda are listed on the Stock Exchange of Hong Kong and will have disclosures in respect of their NPLs. The companies within the Great Wall group and China Orient group have raised public debt and offering circulars in connection with the fundraising provide the information on the operations of the two AMCs respectively.

Chinese specialist bankruptcy courts also draw up the procedures in which the reorganisation takes place. As there were nine specialist courts as at June 2020 (excluding the bankruptcy tribunals),138 I have been selective and focused on only certain of the practices of the specialist courts in Shenzhen and Zhejiang, which are economically advanced regions and which have been the subject of academic commentary.139

1.5.4.2.2.India

In the case of India, I will examine the outcomes of large-scale bankruptcy cases involving Indian companies that have been restructured under the Indian Insolvency and Bankruptcy Code 2016. The primary source of data on the corporate insolvency and resolution processes (CIRPs) will be Debtwire India, the Insolvency and Bankruptcy Board of India and the judgments from the National Company Law Tribunal and the National Company Law Appellate Tribunal. The period in question is 2016 to March 2021. Appendix B, Panel A contains the 12 large accounts which RBI has ordered to utilise the IBC in 2017.140 I collected the data on the large distressed companies that have been resolved under the IBC (as at 31 March 2021) and they are listed in Appendix B, Panel B. The large debtors are those whose claims from financial creditors exceed INR100 million (US$1.3 million) and where the claims cannot be determined, they are excluded from Appendix B, Panel B. Appendix B, Panel B has 154 cases.141

1.5.4.2.3.Hong Kong

For the schemes of arrangement sanctioned by the Hong Kong courts, I identify the publicly listed companies that have undergone debt restructurings via schemes of arrangement for the period 2015–20 from the court decisions, press information and stock exchange filings. The list of filings is found in Appendix C.

1.5.4.2.4.Singapore

The relevant dataset of schemes of arrangement sanctioned by the Singapore courts will be drawn from an earlier study by the author142 (but in this study, I will focus only on the publicly listed companies and/or their subsidiaries), and I have substantially updated the dataset to include the schemes of arrangement up to 31 December 2020. The list of companies is found in Appendix D.

For both Hong Kong and Singapore, I identify the companies that have undergone debt restructuring through press articles, court judgments and stock exchange filings. I also use Perfect Information, a subscription database, and providers of management services for bond restructurings to obtain copies of the explanatory statements or descriptions of the schemes of arrangement. Copies of the shareholder circulars are reviewed in order to ascertain the dilution to the existing public shareholders. More generally, data relating to bond issuance, bank data and macroeconomic data for all four jurisdictions is obtained from Bank of International Settlements, CEIC Data, a subscription database, and Asian Bonds Online.

Chapter two sets the institutional background to, and the development of, restructuring law and practice in the four Asian jurisdictions since the 1980s. Due to constraints of space, the selection is highly selective but illustrates the main drivers and background for the development of the modern restructuring law.

Chapter three analyses the agency costs of the shareholder–creditor and manager–creditor relationships. The chapter first sets the scene on the institutional background of share ownership in the US/UK as well as the four Asian jurisdictions, followed by a section explaining the strategies to deal with the shareholder–creditor and manager–creditor agency costs in the aforementioned jurisdictions. I then explain how the strategies developed in the US/UK will often not work as well in the four Asian jurisdictions in light of differences in their institutional structures. The chapter ends with lessons learned and implications for reform.

Chapter four analyses the agency and coordination costs of creditor–creditor relationships. Similar to chapter three, the chapter first sets the scene on the debt-holdings in the US/UK as well as the four Asian jurisdictions, followed by a section explaining the strategies to deal with the agency costs arising from the different creditors. I discuss the strategies involving the question of deployment of assets and distribution of assets separately. I then explain how the strategies to resolve the conflicts are used in Asia. The chapter ends with lessons and implications for reform.

Chapter five focuses on the NPL problem in Mainland China and India, and the ongoing efforts by the two jurisdictions to utilise the restructuring law to tackle these issues. I argue that the analysis of the standard agency and coordination costs in restructuring proceedings must further consider the use of asset management companies and the consequences of opening up the market to allow greater distressed fund participation.

Chapter six discusses the role of the insolvency practitioner or administrator and the limitations of such roles in the four Asian jurisdictions, including accountability, potential conflicts of interests and effectiveness. The chapter ends with a discussion of lessons learned and implications for reform to remove or mitigate the conflicts and interests and to enhance their effectiveness.